Keywordsnon-financial reporting scientometric analysis social entrepreneurship

JEL Classification L26, A10

Full Article

1. Introduction

The current state of the literature dedicated to social entrepreneurship determines searches regarding the ways in which it differs from other types of entrepreneurship, through the opportunities it creates and the ways of research, the suggestions of conceptual formalization implied by it. The contextualization of entrepreneurship (Welter, 2011) involves a classification of contexts into specific categories, based on the opportunities offered by them to entrepreneurs. Welter (2011) mentioned “such specific categories consist of the historical, temporal, institutional, spatial and social contextual aspect”. The influence of the external context on social entrepreneurship is a little researched field (Estrin et al., 2013), but, in fact, “the purpose of this study is to understand the influence of income inequality and mobility on social entrepreneurship”. In the perspective of the absence of institutional infrastructure, the motivation of social entrepreneurship increases all the more as resources are scarcer and social problems multiply (Stephan et al., 2014). In the same register, the circumstances in which governments exercise their powers, ignoring certain aspects, can trigger a greater “demand” for social entrepreneurship (Dacin et al., 2010).

Being a socially responsible company is much more difficult than ever. Today, the issues are much more diverse and complex, often extended globally, and their data is changing faster than ever. In the age of globalization, it is more difficult for companies to offer unethical business practices, such as unfair labor practices, the exploitation of child and youth labour, environmental pollution, without expecting a clear negative reaction from the general public. To this end, there is increasing pressure on social enterprises to justify their social impact, not only to monitor their performance, but also to acquire resources, strengthen the mission and the overall responsibility of stakeholders (Arvidson and Lyon, 2014). Measuring the impact is increasingly important for creating organizational legitimacy and trust (Luke et al., 2013).

The British legislation has adopted a legislative provision on the establishment of the Community Interest Company (CIC), designed to meet the expectations of the social entrepreneurs, and to create a more favorable environment for public policies, especially in the segment of social enterprises. The shaping of the legislative regulatory space was based on the existing and established modalities, or on mere initiatives, for non-financial reporting. The United Kingdom was not the only European country to create a new legal form for social enterprise. Italy has included in its legislation the so-called “social solidarity cooperative”, specific to social enterprises, and then other European countries, including Spain and France, have acted in a similar manner (Defourny, Nyssens, 2009; 2010). In his article, Nicholls (2009) describes a series of reporting practices used by social entrepreneurs that do not only take into account financial indicators, but also their social or environmental impact. A new theoretical construct is approached, called “mixed value accounting”, which involves an accumulation of reporting logics used by social entrepreneurs regarding their access to resources, as well as the achievement of the objectives of the targeted social mission. First, social impact reporting involves taking into account the ever-changing prospects of these organizations, as well as the demands that come from the authorities or resource providers. Second, mixed value accounting provides a dynamic and multi-level space to optimize reporting practices, but which is not yet an agreed calculation mechanism.

Consequently, the interpretation of an entity's perspective on social impact performance directly affects the calculation method, so this feature will require a review of all reporting procedures. For example, the interpretation of the accounts of a social enterprise is somewhat difficult, because it allocates a share of the profit to their social mission objectives. Therefore, from a standard accounting perspective, many social enterprises do not seem to have financial performance, so they may lose contractual partners to which other private sector companies may be successful.

2. Methodology

Starting from some methods of scientometric analysis, to which we add the systematic review of the literature, we intend to identify:

1. Works/authors with influence in our field of research, using the reference co-citation analysis;

2. The temporal and geographical evolution of the researchers' interest together with the concept of social entrepreneurship and reporting;

3. The reflection in the specific literature of the interconditioning of the concept of social entrepreneurship with non-financial reporting.

2.1. Reference Co-Citation Analysis

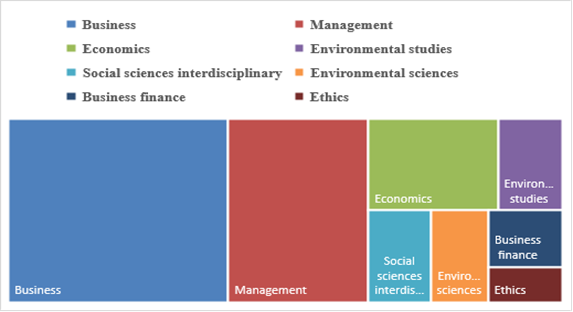

It is one of the most common methods of scientometric analysis by which the publications extracted from the references of the bibliographic databases are selected, which are cited a number of times imposed by a citation threshold. Subsequently, by imposing a citation threshold and the discrimination between significant and insignificant publications, thematic clusters are obtained in the co-citation network that allow us to identify the connotative intellectual structure in the research field (Wu et al., 2020). We sampled our bibliographic database from the Web database of Science Core Collection from where, using the topic “social entrepreneurship” AND “reporting”, from 1990-2020, we extracted 473 publications, and, by choosing the detailed fields in figure 1 and the exclusion of book publications, we reduced it to 283 publications.

Figure 1. Study domains selected in WOS

Source: Own processing

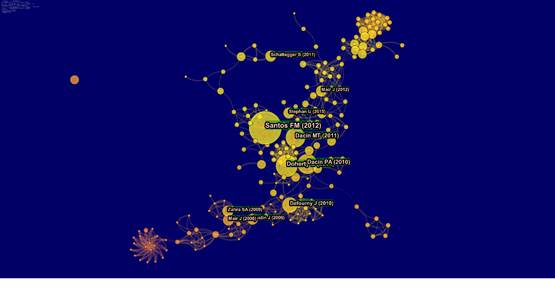

The use of CiteSpace software (5.7. R2, 64 bytes) identified for us 14393 valid references (99.5573%) generating a network (figure 2) made of 658 nodes and 1907 connections, at a threshold of 5 citations per document. The size of the nodes is influenced by the frequency of co-citation of the article / author, and the connecting lines between the nodes by the cooperation relationship between the authors (Chen, 2017). The large size of the node reflects the fact that the document is of great importance in the network.

Figure 2. Bibliometric map based on reference co-citations

Source: Own processing

In table 1, we highlight the first five significant works from the bibliometric network of reference co-citation. We note that the work “A positive theory of social entrepreneurship”, in which Santos proposes a theory aimed at advancing scientific research in social entrepreneurship, has the most co-citations. The author considers that, in order to resolve the tensions that have arisen in the course of their activity, social enterprises apply compromises, such as intentional waiver of profit, to maintain the balance between capturing value and creating value, forcing managers to create a balance between social / welfare logic (value increase) and market / trade logic (value capture). Santos believes thatbringing social entrepreneurship within the area of economic theory we can encompass better, in our theories, “the essence of what it means to be human”.

Table 1. Top 5 important papers

| Authors | Document | Year |

| Santos FM | A positive theory of social entrepreneurship | 2012 |

| Doherty B., Haugh, H., Lyon F. | Social enterprises as hybrid organizations: a review and research agenda | 2014 |

| Dacin TM, Dacin P.A., Tracey P. | Social entrepreneurship: A critique and Future Directions | 2011 |

| Dacin P.A., Dacin T.M., Matear Margaret | Social entrepreneurship: Why We Don't a New theory and How Move Forward From Here | 2010 |

| Defourny J., Nyssens M. | Conception of social enterprise and social entrepreneurship in Europe and the United States: Convergences and Divergences | 2010 |

Source: Own processing

Doherty and co-workers (2014) in “Social Enterprises as Hybrid Organizations: A Review and Research” “make a review of the literature on social enterprise and identify that hybridity is defined by the dual mission of financial sustainability and social purpose as the defining characteristic of social enterprise”. They evaluate the impact of hybridity on the management of social enterprises, the attraction of financial resources. and human resource mobilization and provide a framework for understanding the tensions and trade-offs resulting from hybridity. In the works “Social enterprises as hybrid organizations: a review and research” and “Social entrepreneurship: A critique and Future Directions”, Dacin and collaborators (2010) for the “understanding of social entrepreneurship include the use of theories about creating meaning in the context of social value creation, exploring the motivation and commitment of social enterprises and studying the individual and social processes underlying social entrepreneurship”. Defourny and Nyssens (2010) analyze, from a historical perspective, in the work “Conception of social enterprise and social entrepreneurship in Europe and the United States: Convergences and Divergences”, the social enterprises and social entrepreneurship that they consider to be influenced by the social, economic, political and cultural contexts of the countries in which they appear and notice that, if they are not incorporated into local contexts they will remain only imitations of a formula that will last just as long as they are fashionable.

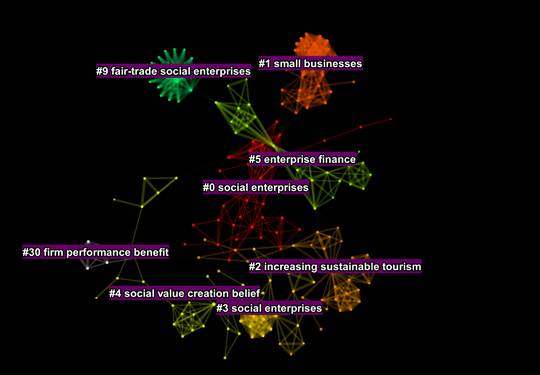

Figure 3. Map of reference co-citation clusters

Source: Own processing

The grouping of similar references generated clusters of co-citation references that highlight the concepts researched by the authors (figure 3). Significant clusters are labelled on the network with the # symbol followed by small numbers. The CiteSpace software uses the probability ratio test (LLR) as extraction algorithms to identify uniqueness and cluster labelling, the document reverse frequency term (TFIDF) to identify and quantify the importance of an existing concept in multiple works, and the mutual information test (MI) for obtaining qualitative information about the research focus in each cluster.

The accuracy of the CiteSpace network is highlighted by silhouette (S) and modularity (Q). The software calculates a global value for S, but for Q both a global value and individual values for each cluster are reported. A Q value close to 1 indicates well-defined clusters and an S value close to 1 indicates confidence in how the nodes were grouped.

As presented in Table 2, the largest cluster (# 0) has 38 members and a silhouette value of 0.917 which indicates good group quality and consistency. The uniqueness of the cluster is labelled by the LLR as that of “social enterprise”, and “performance results” is identified by the TFIDF as the most important concept approached in the studies within the cluster. Qualitative information highlighting the focus of research on certain topics is highlighted by the mutual information (MI) test in Table 2. The second largest cluster (# 1) has 30 members and a silhouette value of 0.984. It is labelled “small business” by the LLR and “informal economy” by the TFIDF.

Table 2. Top 2 representative clusters

| Cluster | Size | Silhouette | TFIDF | LLR | MI |

| 0 | 38 | 0.917 | performance outcomes | social enterprises | non-formal institutional environment (1.43); fair-trade social enterprises (1.42); firm performance benefit (1.42); British social business model (1.42); sustainable development (1.42); fair trade-off (1.42); solar energy (1.42); environmental certification (1.42); institutional theory (1.42); social entrepreneurs life (1.15); content analysis (1.15); hybrid governance (1.15); various sustainability regulation (1.15); Italian social enterprises (1.15); small businesses (1.15); sustainable entrepreneurship (1.15); hybrid nature (1.15); institutional asymmetry explanation (1.15); for-profit social enterprises (1.15); voluntary disclosure (1.15); regulated context (1.15); balancing competing logics (1.15); enterprise finance (1.15); cross-country variation (1.15); tbl concept (1.15); national culture (0.99); growth strategies (0.99); increasing sustainable tourism (0.99); intangible resource (0.99); social venture (0.99). |

| 1 | 30 | 0,984 | informal economy | small businesses | institutional theory (0.1); fair-trade social enterprises (0.09); firm performance benefit (0.09); British social business model (0.09); off-grid pv (0.09); sustainable development (0.09); non-formal institutional environment (0.09); fair trade-off (0.09); small businesses (0.09); institutional asymmetry explanation (0.09); cross-country variation (0.09); hybrid governance (0.05); various sustainability regulation (0.05); Italian social enterprises (0.05); sustainable entrepreneurship (0.05); hidden aspect (0.05); hybrid nature (0.05); for-profit social enterprises (0.05). |

Source: Own processing

2.2. Temporal and Geographical Analysis of Co-Cited References (Bibliographic Coupling)

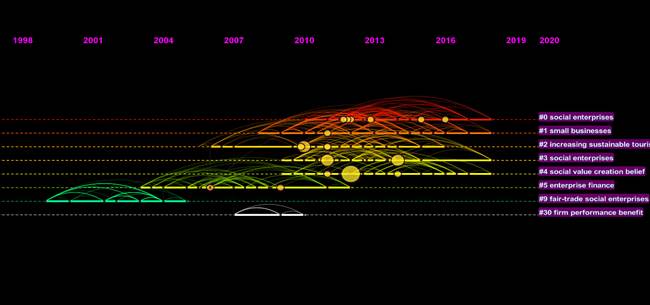

The Space software uses a chronological visualization technique forming a network divided into co-cited reference clusters that allows us to identify the development over time of a concept. Curves of different colours highlight co-citation links, and nodes by size highlight interest in a particular topic. The clusters on the right side of the network are arranged vertically in descending order of importance. In the case of our research, we notice, in figure 4, that the two most important clusters, described above, are those labelled “social enterprise” and “small enterprises”.

Figure 4. Bibliographic coupling analysis 1998-2020

Source: Own processing

The interest of researchers to study the concept of “social enterprise” manifested itself over a period of 8 years (2010-2018), an interest overshadowed by the study of the concept of “small business” over a period of 11 years (2007-2018). The maximum point of interest from the researchers was registered by the concept “social value creation belief” in 2011-2012, highlighted by the size of the graphic node.

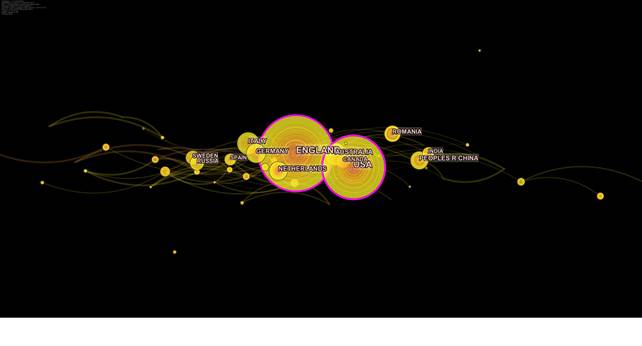

Figure 5. Analysis of co-citations at country level

Source: Own processing

The researchers with the highest number of reference co-citations (figure 5) were from England (56 co-citations), USA (47), Australia (18), Italy (17), PEOPLES R CHINA) (17).

2.3. Interconditioning the Concept of Social Entrepreneurship with the Non-Financial Reporting

For this approach, we re-interrogated the Web of Science Core Collection database, using the syntax with Boolean operators “social entrepreneurship” AND “reporting”, which resulted in 45 articles in the fields of business, management, economics, and environmental sciences. Adapting the idea taken after Bansal (2019), we formulated three classification criteria (table 3) in terms of content for selected articles, taking into account both the themes and details revealed in the literature on social entrepreneurship and its reporting, financial, or non-financial, as well as the methodologies for putting into practice the social entrepreneurship according to the literature.

Table 3. Criteria for comparing the contents of selected items

| I. Types of content of the articles / Types of research proposed in the selected articles | II. Expression of social entrepreneurship (AS), pre-established compliance categories. | III. Expression of Non-financial reporting (NFR), pre-established compliance categories |

| a) literature study, | a) yes | a) financial and non-financial reporting; (both) |

| b) empirical with elements, both of qualitative type and of quantitative type; | b) mostly_yes | b) Obvious non-financial reporting (non-financial) |

| (partially yes) | ||

| c) qualitative empirical; | c) mostly_no | c) It does not provide any information in the sense of either of the 2 types of reports |

| (partially no) | (does not answer) | |

| d) quantitative empirical, | d) no |

Source: Own processing

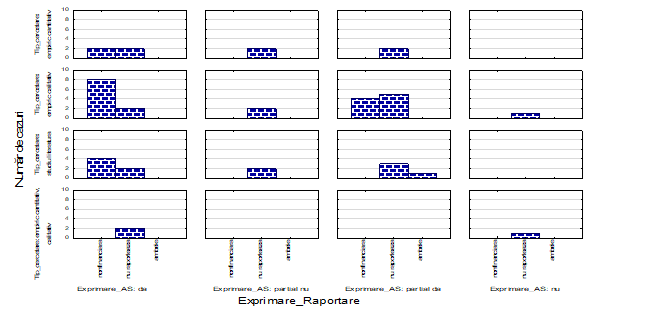

Considering the criteria in table 3 as the research variables (the dependent variable is I Types of content of the articles / Types of research proposed in the selected articles, and the independent variables are II. Expression of social entrepreneurship (SA) and III. Expression of non-financial reporting (NFR)) graphically processed the connection between the frequencies of occurrence of the variables (figure 6).

Figure 6. Comparison of variables I.Types of contents of articles with II.Expression of social entrepreneurship (SA) and with III. Expression of non-financial reporting (NFR).

Source: Own processing

- The highest simultaneous frequency recorded is, with 8 cases (articles), the coincidence between quantitative empirical study-clear, dominant expression of SA-clear expression of NFR (I.c with II.a. with III.b.);

- The second high frequency recorded simultaneously is, with 5 cases (articles), the coincidence between I.c. and II.b. with III.c. (qualitative empirical study-sufficient but not dominant expression of SA-non-expression of any of the NFR reporting modalities);

- The 3rd and the 4th simultaneous high frequency recorded are, with 4 cases each (articles), the coincidence between:

- I.c. with II.b. with III.c. (qualitative empirical study - sufficient but not dominant expression of AS - clear expression of NFR);

- I.a with II.a. with III.c. (literature study - clear, dominant expression of SA - clear expression of NFR);

Social entrepreneurship appears as a priority, in articles whose content is empirically qualitative or literature study, consistent with articles in which non-financial reporting appears clearly or fairly clearly outlined theoretically. Non-financial reporting appears in the same types of articles as social entrepreneurship, so both the first notion (SA) and the second (NFR) coincide, practically, in the approaches in the articles.

3. Conclusions

The aim of our study was to identify, through a scientometric approach, the evolution of the concepts of social entrepreneurship and non-financial reporting and to identify how the interconditioning between the two concepts is reflected. Using the bibliometric method “reference co-citation analysis” we identified the authors who created the scientific basis that was the starting point for further research:

- Santos (2012) conceptualizes the normative values of “social entrepreneurship and analyzes the definitions of what is social and how it can be evaluated”;

- Dacin and colleagues (2010; 2011) analyzed “37 definitions of social entrepreneurship, find that the common denominator that defines social entrepreneurship is the creation of social value”;

- Doherty et al. (2014) identified that hybridity, defined by the “dual mission of financial sustainability and social purpose, is the defining characteristic of social enterprises”.

- Defourny and Nyssens (2009; 2010) identified that social enterprises and social entrepreneurship are influenced by the social, economic, political and cultural contexts of the countries in which they occur.

Nonetheless, social entrepreneurship does not have a consistent theoretical support, based only on reporting to the paradigm, the researchers of social entrepreneurship being in the middle of a series of debates involving the description and conceptual clarity, the delimitation of the boundaries of social entrepreneurship and the identification of valuable research questions.

Clustering the database through the CiteSpace software allowed us to identify 2 concepts that roused the interest of researchers:

- “Social enterprise” was the concept studied over 8 years (2010-2018);

- “Small business” appeared in research studies over a period of 11 years (2007-2018).

Chronological processing of the database revealed that most studies addressing social entrepreneurship came from developed economies - England, USA. Regarding the interdependence of social entrepreneurship with non-financial reporting, the lack of standardization in the reporting of social enterprises creates difficulties for social entrepreneurs regarding the way of reporting the newly created value to the external public.

References

- Arvidson, M. and Lyon, F., 2014. Social impact measurement and non-profit organisations: Compliance, resistance, and promotion. International Journal of Voluntary and Nonprofit Organizations, 25(4), pp. 869-886.

- Bansal, S., Garg, I. and Sharma, G., D., 2019. Social Entrepreneurship as a Path for Social Change and Driver of Sustainable Development: A Systematic Review and Research Agenda, Sustainability, 11, pp. 1091-1121.

- Chen, C., 2017. Science Mapping: A Systematic Review of the Literature. Journal of Data and Information Science, 2(2), pp.1–40.

- Dacin, P. A., Dacin, M. T. and Matear, M., 2010. Social entrepreneurship: Why we don’t need a new theory and how we move forward from here. Academy of Management Perspectives, 24 (3), pp. 37-57.

- Defourny, J. and Nyssens, M., 2009. Social enterprise in Europe: Recent trends and developments. Social Enterprise Journal, 4 (3), pp. 202-228.

- Defourny, J. and Nyssens, M., 2010. Conceptions of Social Enterprise and Social Entrepreneurship in Europe and the United States: Convergences and Divergences. Journal of Social Entrepreneurship, 1(1), pp. 32-53.

- Doherty, B., Haugh, H. and Lyon, F., 2014. Social entreprises as hybrid organizations: A review and research agenda. International Journal of Management Reviews, 16, pp. 417-436.

- Estrin, S., Mickiewicz, T. and Stephan, U., 2013. Entrepreneurship, social capital, and institutions: Social and commercial entrepreneurship across nations. Entrepreneurship Theory and Practice, 37(3), pp. 479-504.

- Luke, B., Barraket, J. and Eversole, R., 2013. Measurement as legitimacy versus legitimacy of measures: Performance evalution of social entreprise. Qualitative Research in Accounting and Management, 10 (3/4), pp. 234-258.

- Nicholls, A., 2009. 'We do good things, don't we?': 'Blended Value Accounting' in social entrepreneurship. Accounting Organizations and Society, 34 (6/7), pp. 755-769.

- Santos, F.M., 2012. A positive theory of social entrepreneurship. Journal of Business Ethics, 111(3), pp. 335-351.

- Stephan, U., Uhlaner, L. M., Stride, C., 2014. Institutions and social entrepreneurship: The role of institutional voids, institutional support, and institutional configurations. Journal of International Business Studies, 46, pp. 308-331.

- Welter, F., 2011. Contextualizing entrepreneurship: Conceptual challenges and ways forward. Entrepreneurship Theory and Practice, 35(1), pp. 165-184.

- Wu, H., Zhao, Z., Xue, X., Shen, G.Q. and Yang, R.J., 2020. An Integrated Scientometric and SNA Approach to Explore the Classics in CEM Research. Journal of Civil Engineering and Management, 26 (5), pp.459-474.

Article Rights and License

© 2020 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.